Penny-Foolish, Pound-Wise: The Other Half

This is the follow-up to a previous post that listed 12 ways to be penny-foolish. These tips are most relevant for a US cost-of-living breakdown.

"Pound-wise" is, of course, the other half of being penny-foolish/pound-wise, but most of this is widely covered on various finance blogs. Instead, I'll elaborate on only my particulars. I can't really call this advice, since I don't really advise anyone to try these things, since they're weird and unworkable for most people.

Still, if you can pull them off, even temporarily, the gains are large.

Find the Pounds

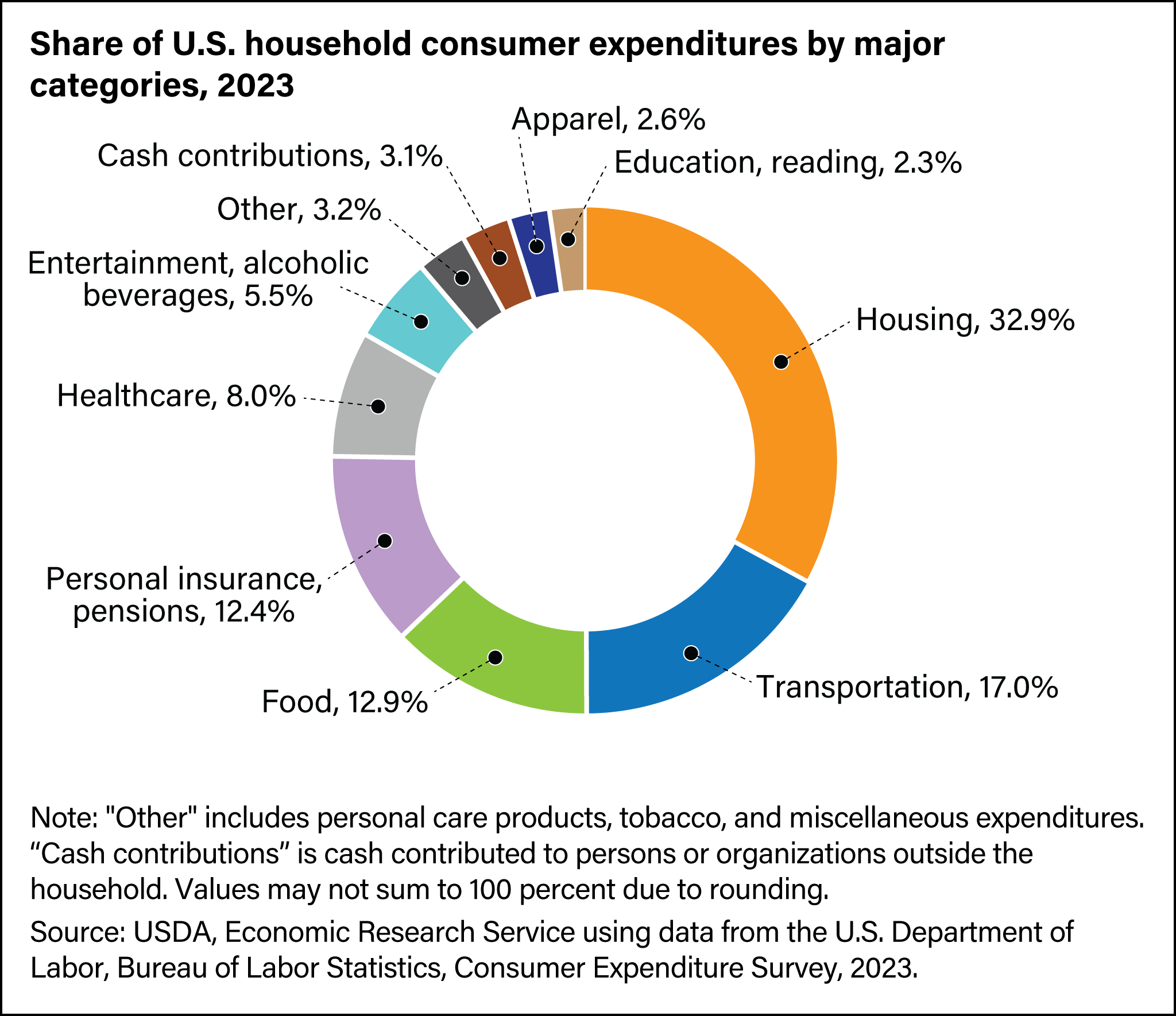

To be wise about pounds, first you need to know what they are. Below is an illustrative chart.

Housing

This will almost always be your largest expense, and in big cities, it will dominate overall.

It's easier said than done, but my savings strategy has been more to avoid paying rent entirely rather than finding especially budget accommodation for the long-term. How to avoid paying rent? My methods:

- Get work to pay for it - For me, this started in university as a resident advisor. After graduation, I lived and worked at a factory with dorms for the workers, then lived in the spare room of my boss. Later, when working on a startup, I lived in the spare room of an investor. Neither my old boss or investor would have written me an additional $1000+ check each month, but they didn't mind letting me avoid that much in rent.

- Mooch/Scrounge - Generally, this involves asking around and seeing where there is space. You usually need backup accommodation, which could be a friend's couch, a cheap hotel, or camping. To avoid wearing out your welcome, best if you're not in a co-occupied space long term, but that still leaves out-of-town friends' places, empty offices, and other spaces (I get a cheap mattress delivered from Amazon). One thing that helps with mooching is being very generous with your own place whenever you happen to have one. (I used pastecal.com to make a calendar for my friends to book themselves into my spare room.)

- Be willing to travel - This is beneficial because you can live somewhere cheaper, or just travel to whatever free accommodation pops up. A flight might be a few hundred dollars, but this can easily pay for itself in a few nights of avoided rent.

Taxes

Avoid, not evade, taxes. The fact that this is even slightly unseemly means it’s probably under-utilized, but most of the tax avoidance you’ll do is actually the government trying to incentivize you! Tax is taxes ~1/3 of your gross income, so this is certainly a pound, not a penny.

The main tax savings come from using your retirement accounts: an IRA and a 401(k) save you taxes now, and the Roth versions save you taxes later. With these, you'll avoid tax and take advantage of the miracle of compound interest. Compound interest is so powerful that if done right (hint: a low-fee index fund), it will dwarf all other financial decisions, becoming the only pound-wisdom really necessary. Make these savings as automatic as possible, ideally by having them taken directly from your paycheck.

That said, some people do go overboard pinching pennies when they're young and poor, when the marginal value of money is high. You'll have to find some middle ground, but you can solve your retirement savings problem entirely by temporarily saving aggressively when you're making OK money but still relatively young, say late 20's through 30's.[1]

Healthcare

If you've got healthcare through work, great. I often didn't, so here's my historical approach:

- Get a low-premium, high-deductible healthcare plan, and keep enough in savings to cover your deductible.

- Learn to diagnose/treat yourself (sounds dire, but it's a useful skill to have anyway, and it's easier now with LLMs).

- Get a short-term plan or travel insurance that can still cover some time at home. If you're otherwise without, this can be used to cover short-term, high-risk activities like a wilderness camping trip.

- Be as healthy as possible, do this by 1. not smoking (hopefully self-explanatory) 2. eat decently and get enough sleep, you'll get sick less, and 3. exercise (safely), which I've found on net reduces orthopedic injuries, e.g., twisting an ankle.

Debt

Among the worst money pits, think of it as a reverse investment. An interest rate on debt is as bad as that same rate on an investment would be good. The most obvious debt to avoid is credit cards, which have a guaranteed rate in the teens (which would be spectacularly good as an investment, but bad as a debt) because so many people default on them. Unless you plan to negotiate or default, you're subsidizing everyone else who does.

Get a cash-back credit card and automatically pay it off every month. I use the Fidelity 2% rewards, Capital One Quicksilver 1.5% (no forex fees when abroad), and the Amazon Prime 5% back Visa for Amazon purchases only (assuming you have Prime, as I finally do now after mooching off my brother's account for ~2 decades).

Cars

Ideally, avoid having a car altogether, but if you must, get one that offers good value. Toyotas run better than Mercedes, and as Paul Fussell describes in his classic Class, expensive cars actually signal the opposite class status of what you'd naively expect:

If your money and freedom and carelessness of censure allow you to buy any kind of car, you provide yourself with the meanest and most common to indicate that you're not taking seriously so easily purchasable and thus vulgar a class totem

Career and Hobbies

- Increase your income or savings rate, this usually looks like moving cities or jobs. I've lived in about a dozen cities and worked in a number of fields, and one thing that's underrated amongst those who've moved around less is just how different stuff can be. The same job in a different field or location can pay wildly differently, so optimizing can have huge payoffs.

- Get ROI on your education - This seems more in the public consciousness today than when I was in school, but if you’re going to pay hundreds of thousands for a degree, probably pick one that pays.

- Avoid expensive hobbies - Boating, flying, smoking, gambling (insert your favorite "actually skiing/wine/golf etc. isn't really that expensive" here)

- Common advice is to audit your subscriptions, which do add up. One step better is to make any new subscription you get default-cancel and time-limited instead of default-renew and indefinite. Get a free one-time use card service. I use Privacy.com. Anytime you want to start a trial of something, use a one-time-use card and change it later if you end up using it.

Be a Recipriocal Mooch

You may have noticed a theme here: I am mooching off of those around me. This would be bad and parasitic if I didn't reciprocate at all, but with reciprocation, it is net good for everyone involved. Further, just the act of trading back and forth in good faith with people you know strengthens and deepens those relationships. We're saving money and having fun!

This will be harder for women who want children, so are on compressed timelines. ↩︎